Household Budgeting: Simple Tools That Actually Work

You don't need complicated software. We show you practical methods for tracking expenses, setting savings goals, and using Czech bank tools to improve your financial situation.

Why Budgeting Matters More Than You Think

Let's be honest — most people avoid budgeting. It sounds boring, restrictive, and painful. But here's the thing: you're already spending money. A budget doesn't control you. It just tells you where your money's actually going.

Whether you're saving for a vacation, paying off debt, or just trying to understand your finances, budgeting gives you control. And in the Czech Republic, where banking options have expanded dramatically in recent years, you've got tools that make this easier than ever before.

The reality: Most Czech households don't track their spending. Those who do typically save 15-25% more annually simply by seeing where money goes.

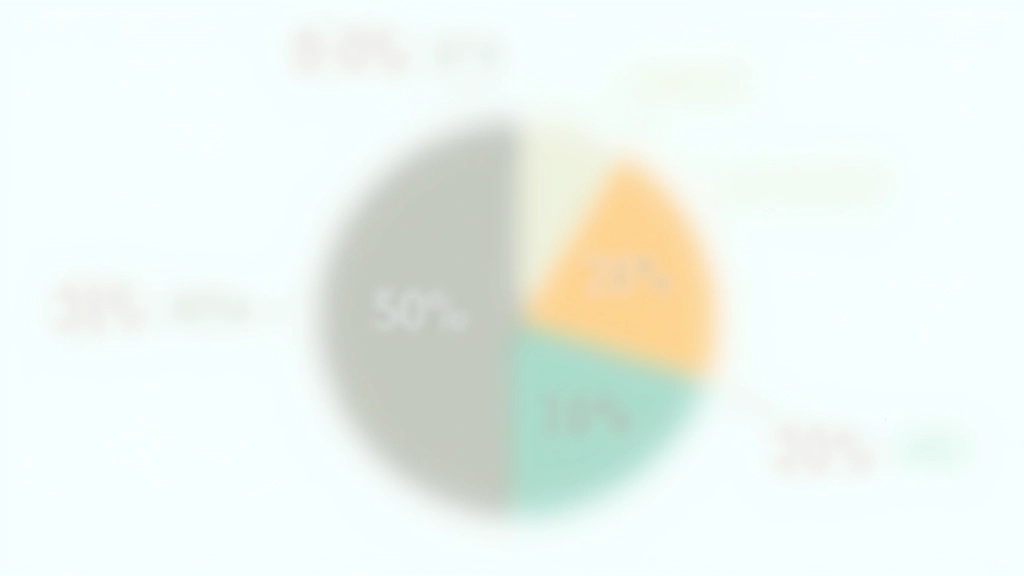

The 50/30/20 Rule: Start Here

This isn't complicated. It's literally three categories:

- 50% Needs — Rent, utilities, groceries, insurance. Things you can't live without.

- 30% Wants — Dining out, hobbies, streaming services, clothes. The fun stuff.

- 20% Savings — Emergency fund, retirement, paying down debt. Your future self.

If you're spending 70% on needs and wants, you've got 30% for savings. That's actually realistic for most Czech households. And if you're not there yet? That's your signal. Something needs to change — and now you know what.

Tools That Actually Work (No Subscriptions Required)

Spreadsheet (Google Sheets)

Seriously. A simple spreadsheet with months across the top and expense categories down the left side works better than you'd think. You'll see spending patterns in seconds. Plus it's free, it syncs across devices, and you control everything.

Pro tip: Use conditional formatting to highlight months where you overspend. Visual cues work.

Czech Bank Mobile Apps

Most Czech banks (Česká spořitelna, ČSOB, Komerční banka, Monzo) now offer spending categorization in their apps. Your bank already knows where you're spending. Let it help you. You'll see groceries, transport, restaurants all separated automatically.

Reality check: It's not perfect, but it's good enough to spot trends.

Envelope Method (Digital Version)

This old technique works because it forces discipline. Open a separate savings account for each goal (emergency fund, vacation, car repair). When you get paid, split money into envelopes immediately. You can't spend what you don't see in your checking account.

Why it works: Psychological barrier. Moving money to savings feels more final than just "deciding" to save.

The Tracking That Sticks: Monthly Check-Ins

You don't need to log every purchase. That's tedious and you'll quit. Instead, spend 30 minutes on the last day of each month reviewing what you actually spent. Pull your bank statements. Check your app. See where you were surprised.

Ask yourself three questions: Did I overspend on wants? Did I miss any categories? What'll I do differently next month? That's it. One conversation with your money per month. Most people find patterns emerge in about three months.

Some months you'll spend more on groceries because you hosted dinner. Some months transport costs jump. That's normal. The budget isn't about being perfect. It's about being intentional.

Savings Goals That Feel Real

Here's where budgeting gets actually useful. Once you know your spending, you can build real savings. Not "I want to save more" — specific targets with timelines.

Example: Building a 3-Month Emergency Fund

Say your monthly needs (rent, utilities, food, insurance) total 30,000 CZK. An emergency fund covers 3 months: 90,000 CZK. That feels overwhelming until you break it down. If you can save 3,000 CZK per month, you'll have it in 30 months. That's 2.5 years. Realistic? Absolutely.

Now you know: 3,000 CZK per month goes to the emergency fund. It's not a suggestion. It's a line item in your budget. Once that's done, redirect that 3,000 to another goal — maybe retirement, maybe home repairs. You've already proved you can do it.

Important Note

This article is informational and educational. The 50/30/20 rule and budgeting methods described are general frameworks. Your personal situation may require different allocations — especially if you're managing debt, have dependents, or live in high-cost areas. Consider consulting with a financial advisor for personalized guidance. Bank features and interest rates mentioned are current as of April 2026 and may change.

You've Got This

Budgeting doesn't mean deprivation. It means knowing what you're doing with your money instead of wondering where it went. Start with the 50/30/20 rule. Pick one tool — spreadsheet, your bank app, or separate accounts. Spend 30 minutes once a month checking in.

That's genuinely enough to change your financial life. You don't need perfect. You need to start.

Related Articles